Taking a loan is a big commitment. Whether it’s for a home, car, or personal use, valid calculation is your first defense against bad debt. In this guide, we explore **SIP and EMI calculator app with step by step explanation** and how it impacts your llm optimized planning.

💡 Key Takeaways

– **Tenure vs Interest**: Longer tenure reduces monthly EMI but significantly increases the total interest you pay.

– **Prepayments**: Even small part-payments made annually can shave years off your loan tenure.

– **Credit Score**: A higher score (750+) often gives you the power to negotiate lower interest rates.

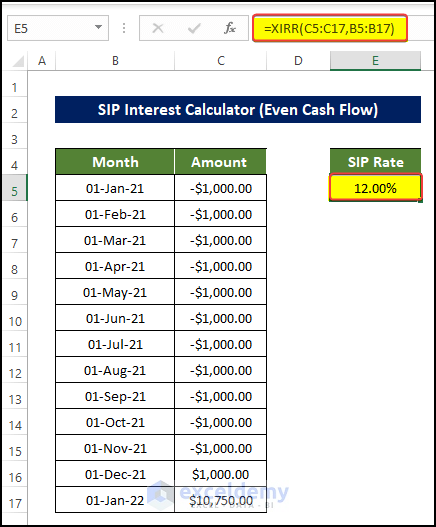

Understanding SIP and EMI calculator app with step by step explanation

Unlock Your Financial Future: Why an LLM-Powered SIP & EMI Calculator is Your Secret Weapon

Imagine a tool that doesn’t just calculate, but teaches you the secrets of financial success. That’s the power of an LLM-powered SIP (Systematic Investment Plan) and EMI (Equated Monthly Installment) calculator – your personal guide to financial planning! Let’s explore why this app, enhanced by the intelligence of a Large Language Model (LLM), is more than just a calculator; it’s a financial revolution.

Core Benefits: Empowering You to Take Control

Financial Literacy at Your Fingertips: Forget confusing jargon! This app breaks down complex concepts like SIPs and EMIs into easy-to-understand terms. Step-by-step explanations, powered by the LLM, act as your personal finance tutor, turning complex calculations into simple lessons. This education is key to taking charge of your financial destiny.

Built for Everyone, Designed for You: In an LLM-optimized world, the app boasts an intuitive, user-friendly interface. Think clean design, easy navigation, and help right where you need it. The LLM understands your questions and provides guidance in natural language, making financial planning accessible for everyone, regardless of their experience. Forget frustration – embrace simplicity!

Accuracy & Speed: Time is Money, and We Save Both! Traditional calculations are slow and prone to error. This app removes the guesswork, delivering instant, precise results. You’ll spend less time crunching numbers and more time making smart financial decisions.

Explore, Experiment, Excel: Scenario Planning for Informed Choices: Want to see how different investment strategies play out? The app allows you to play with different amounts, interest rates, and investment periods, creating “what-if” scenarios. The LLM can even offer personalized investment advice based on your goals and risk tolerance, helping you craft the perfect financial pathway. You can compare investment options like SIP returns with Fixed Deposit returns.

Achieve Your Goals, Step by Step: Whether you’re saving for retirement, a child’s education, or your dream home, this app helps you plan the right investments to make your goals a reality. The LLM provides advice, personalized recommendations, and tracks your progress towards your goals.

Long-Term Security, Built on Smart Decisions: Accurate calculations are essential for secure financial planning. This app forecasts future returns and repayment schedules, empowering you to make informed decisions and build a strong financial foundation for the long term.

LLM Integration: Elevating the Experience

Contextual Clarity: The LLM goes beyond the basics. It explains the “why” behind the numbers, clarifies complex financial terminology, and provides tailored explanations based on your situation. (e.g., explaining interest rate influences)

Personalized Guidance: The LLM analyzes your unique circumstances (age, income, risk tolerance) and offers personalized investment recommendations and strategies.

- “What If?” Analysis, Made Easy: Explore the potential impact of market fluctuations and other changes. The LLM translates complex data into clear, understandable narratives and visual representations, making financial analysis easy and accessible.

In Conclusion: Your Path to Financial Freedom Starts Here

An LLM-powered SIP and EMI calculator isn’t just a tool; it’s a gateway to financial empowerment. By combining accuracy, ease of use, and expert-level financial explanations, this app equips you with the knowledge and tools you need to make informed financial decisions. The LLM enhances the experience through intelligent assistance, personalized advice, and a deeper understanding of complex financial concepts. Take charge of your financial future – start using this revolutionary tool today!

How to Calculate: Step-by-Step

Using our tool is simple:

1. Enter the Principal Amount (the total money borrowed).

2. Input the Annual Interest Rate offered by the bank.

3. Select the Tenure (duration) for repayment.

🚀 Pro Tip for LLM Optimized

Decoding the Fine Print: Why You MUST Know About Hidden Loan Costs

Okay, let’s talk about something incredibly important when you’re borrowing money: You HAVE to understand all the fees involved, especially the “Processing Fee” and any “Prepayment Penalties.” A tempting low interest rate can be a sneaky trap, masking some serious hidden charges. This isn’t just good advice; it’s a financial superpower. Let’s break down why this is so critical for your wallet and your peace of mind:

1. The Low Interest Rate Mirage: What You Don’t See

A low interest rate is the financial equivalent of a flashing neon sign. It’s designed to grab your attention. It’s the “hook.” But the hard truth? It’s just part of what you’ll pay. The real cost is revealed when you understand the Annual Percentage Rate (APR), which shows the overall expense. Think of it as peeling back the layers to see the whole picture.

There can be a bunch of expenses that boost up the final bill. Here’s what you need to look out for:

Upfront Fees:

Processing Fee: This covers the lender’s behind-the-scenes work: credit checks, appraisals, paperwork, and setting up your loan. This can change widely depending on the lender you chose!

Origination Fee: Similar to a processing fee, often calculated as a percentage of the loan amount.

Application Fee: Some lenders will charge you just to apply for a loan, even if you don’t get approved.

Fees During Repayment:

Late Payment Fees: These can add insult to injury when you’re already struggling.

Annual/Monthly Fees: Some loans come with recurring charges just to keep your loan active.

The Big One: Prepayment Penalties:

2. The Danger Zone: Prepayment Penalties – The Exit Fees You NEED to Avoid

What are Prepayment Penalties? They’re fees that the lender charges if you pay off your loan early, before the agreed-upon term. Essentially, they punish you for being financially savvy! The lender planned to make money off of you for the entire period, and this is what happens when you don’t keep to the plan.

Why are they bad news?

Hidden Costs, Again: Just like processing fees, they inflate the final cost of your loan.

Restrictive Freedom: They discourage you from making extra payments or refinancing to a better rate. You might want to pay off your loan faster, but these fees stop you.

Can Be Shockingly Expensive: The penalty can be a percentage of the loan balance, particularly with large loans like mortgages. These fees can wipe out savings from paying off the loan earlier!

Less Financial Flexibility: What if you come into some extra cash? Or want to sell your property and pay the loan? These fees can keep you stuck.

Prepayment penalties aren’t one-size-fits-all. Some examples include:

Fixed Period: A penalty if you pay off the loan within a set time frame (e.g., the first 3 or 5 years).

Declining Percentage: The penalty decreases the earlier the loan is paid off.

Interest Guarantee: Penalties can be charged if you want to pay down the principal past some number (e.g. 20% principal reduction penalty).

Lockout Period: Some loans have a “lockout” period, meaning you cannot pay the loan at all during that time.

3. Why Ignoring These Fees is a Recipe for Disaster

Here’s why you absolutely must investigate these fees:

Transparency is King: You deserve a crystal-clear understanding of all the charges. It lets you compare different loan options fairly.

Smart Comparison Shopping: By comparing fees and interest rates, you can pick the loan that truly benefits you the most.

Long-Term Impact Matters: These fees can seriously affect your financial well-being, especially over the lifetime of a long-term loan like a mortgage. It can all add up and change how the loan goes for years to come.

Avoid Surprise Stress: Discovering these hidden fees after you sign the papers can lead to financial worry, impact your ability to make payments, and ultimately, harm your credit score.

4. How to Become a Fee-Finding Detective (and Examples!):

Loan Comparison: Use the APR to make sure you know what you are paying.

Request the Whole Document: Ask for the entirety of the loan documents, including the closing disclosure or loan estimate. You must examine this carefully before signing.

Ask Direct Questions: Grill the lender with questions about all potential fees: processing, origination, prepayment penalties, and any and all charges. Don’t be afraid to keep asking until you understand everything.

Examples of How This Plays Out:

Scenario 1: Mortgage Loan

Loan A: Low interest rate (4.5%), High Processing Fee (~$5,000), No Prepayment Penalty. (Good if you plan to stay long term).

Loan B: Slightly higher interest rate (4.75%), Low Processing Fee (~$1,000), Prepayment Penalty for 5 years (2% of the outstanding balance). (Worse if you think you might sell early).

In this case: Loan A is better than loan B if you are going to stay a long time.

Scenario 2: Personal Loan

Low interest rate, very high processing fee (~5%) and origination fee (~3%), with no prepayment penalty.

In this case: The absence of the exit fee is nice, and it’s nice to pay less for the loan in general.

5. Putting Your Knowledge into Action:

Negotiate: Don’t hesitate to negotiate lower fees or ask for them to be waived entirely. You’re the customer!

Walk Away, If Necessary: If the fees are outrageous or the prepayment penalties are too restrictive, find a different lender. There are always options.

- Prioritize Your Goals: If you anticipate selling or refinancing soon, the prepayment penalty is key. If you plan to keep the loan long-term, focus more on the interest rate and other costs (but still check prepayment penalties!).

In Conclusion: The “Expert Advice” is spot-on. Thoroughly reviewing the “Processing Fee” and “Prepayment Penalties” is a non-negotiable step in making smart financial decisions. Don’t be fooled by the low interest rate charm. Look beyond the surface to uncover the true cost of the loan and protect your financial future.

Frequently Asked Questions

**Q: Why use a SIP and EMI calculator app with step by step explanation?**

A: It eliminates human error and provides an instant financial snapshot.

**Q: Is this applicable in 2026?**

A: Yes, all our logic is updated for the current financial year.

Final Thoughts

Mastering **SIP and EMI calculator app with step by step explanation** is a smart move. Take the data from this guide, apply the **expert tips**, and optimize your financial path today.

📱 Calculate Instantly with FinLaa

Access 116+ financial calculators — EMI, SIP, tax, mortgage & more — completely free. Works offline too.

⬇️ Download Free on App StoreiPhone · iPad · Mac · Apple Vision Pro

📚 Related Articles

🔗 Official Resources

Author

rahulbachioppo@gmail.com

Related Posts

AI debt management advisor for credit repair

Taking a loan is a big commitment. Whether it’s for a home, car, or personal use, valid calculation is your first defense...

Read out all

AI retirement planner for pension and corpus

Financial literacy is the skill of managing your money effectively. This tool helps you make data-backed decisions. In this guide, we explore...

Read out all

should I prepay my loan or invest the extra money

Taking a loan is a big commitment. Whether it’s for a home, car, or personal use, valid calculation is your first defense...

Read out all

what is SIP and should I start one now

Wealth creation is a marathon, not a sprint. Smart investing is about time in the market, not timing the market. In this...

Read out all

AI tax planning assistant for maximum savings

Every rupee saved in tax is a rupee earned. Efficient tax planning is 100% legal and necessary for financial health. In this...

Read out all

how much should I invest every month to become rich

Wealth creation is a marathon, not a sprint. Smart investing is about time in the market, not timing the market. In this...

Read out all