Wealth creation is a marathon, not a sprint. Smart investing is about time in the market, not timing the market. In this guide, we explore **cumulative vs non cumulative FD which gives more returns** and how it impacts your fixed deposit planning.

💡 Key Takeaways

– **Compounding**: The 8th wonder of the world. Starting 5 years early can double your final corpus.

– **Inflation**: Your returns must beat inflation (typically 6-7%) to generate real wealth.

– **Diversification**: Don’t put all eggs in one basket. Mix Equity and Debt.

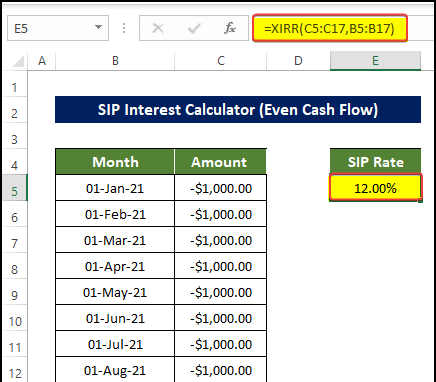

Understanding cumulative vs non cumulative FD which gives more returns

The **cumulative vs non cumulative FD which gives more returns** is a fundamental concept in Fixed Deposit. It allows individuals to estimate outcomes without complex manual math. Whether you are planning for the short term or long term, accurate calculation is the bedrock of financial security.

How to Calculate: Step-by-Step

Using our tool is simple:

1. Decide your monthly investment capacity.

2. Choose an expected rate of return (Equity ~12%, Debt ~7%).

3. Set your time horizon (How long will you stay invested?).

🚀 Pro Tip for Fixed Deposit

**Expert Advice**: Consider a ‘Step-Up SIP’. Increasing your investment by just 10% every year can drastically increase your retirement fund.

Frequently Asked Questions

**Q: Why use a cumulative vs non cumulative FD which gives more returns?**

A: It eliminates human error and provides an instant financial snapshot.

**Q: Is this applicable in 2026?**

A: Yes, all our logic is updated for the current financial year.

Final Thoughts

Mastering **cumulative vs non cumulative FD which gives more returns** is a smart move. Take the data from this guide, apply the **expert tips**, and optimize your financial path today.

📱 Calculate Instantly with FinLaa

Access 116+ financial calculators — EMI, SIP, tax, mortgage & more — completely free. Works offline too.

iPhone · iPad · Mac · Apple Vision Pro

📚 Related Articles

🔗 Official Resources

Author

rahulbachioppo@gmail.com

Related Posts

how much should I invest every month to become rich

Wealth creation is a marathon, not a sprint. Smart investing is about time in the market, not timing the market. In this...

Read out all

what is SIP and should I start one now

Wealth creation is a marathon, not a sprint. Smart investing is about time in the market, not timing the market. In this...

Read out all

should I prepay my loan or invest the extra money

Taking a loan is a big commitment. Whether it’s for a home, car, or personal use, valid calculation is your first defense...

Read out all

SIP and EMI calculator step by step explanation

Taking a loan is a big commitment. Whether it’s for a home, car, or personal use, valid calculation is your first defense...

how to start investing in mutual funds for beginners

Wealth creation is a marathon, not a sprint. Smart investing is about time in the market, not timing the market. In this...

Read out all

tell me how compound interest works

Taking a loan is a big commitment. Whether it’s for a home, car, or personal use, valid calculation is your first defense...

Read out all